Many of my blogs focus on investing, so I changed tact for this one.

The reason for this is because of three things I have come across recently:

- An article highlighted an investor who had over £200,000 in a pension they managed, and now it is worth just over £3,000 due to the investment decisions made.

- An article in a specialist investment paper indicated that the FCA wanted to remove the percentage charging structure by financial planners.

- A financial planning practice where a family made up 25% of the fee income of that practice and was paying over £200,000 per annum.

When looking for research into the value of a financial planner, everything points to Vanguard Research carried out in 2020, which highlighted the following:

Like everything, this should be put in context, and the critical element is understanding the role of a financial planner. It is also worth understanding where the FCA is coming from on this.

FCA

The FCA are the Financial Conduct Authority and oversees approved financial service businesses. The critical change that has come in is Consumer Duty. This is about protecting the consumer and ensuring they do not suffer harm. Of course, the client must take some responsibility for their actions. Still, whether it is someone providing advice or products, they should take an element of responsibility for what they offer.

As with any article, the truth is often different to the headlines. Having spoken to the FCA on fees, this is the context:

- A financial planner can charge any fee they want. However, this must be “reasonable and fair.” Significantly, whatever is offered within the service proposition should be documented and delivered, particularly regarding annual reviews.

- Is there a cross-subside between clients paying high fees and those who are not? In the discussions with the FCA, they accept this may happen, but it goes back to the first point: is it reasonable and fair, and more importantly, can it be evidenced?

- Does the FCA want to remove the percentage charging structure? In my discussion, they indicated that they were not setting out to control the fee structure, but again, it comes down to being fair and reasonable.

On that basis and looking at the points at the start of this article:

- Clearly, the article in the trade paper needs to be corrected and aims to generate fear and anger within the financial planning community. This doesn’t help anyone.

- Is a fee for a family of over £200,000 fair, especially when it makes up a large proportion of the overall fee income? Well, that depends.

The value of a financial planner

Perhaps taking out the word “value” is an excellent place to start.

In the past, financial advisers “sold” a product and the investments that came with that. It is probably fair to say that if there has been no interaction with that adviser since the product was sold, someone is paying for something that may no longer be appropriate for their needs.

Platforms such as Hargreaves Lansdown and Interactive Investor serve a purpose. For those who want to manage their own money, these are ideally placed as a cheap alternative to a financial planner.

However, taking this route, the investor must remember that the responsibility for the research and their action rests with them. Take Woodford as an example; you can blame Hargreaves Lansdown for promoting the strategy, but ultimately, the decision to invest came from the client because they chose not to take any advice (and, of course, you can argue that some advisers did select this fund).

Taking the first point at the start, although it is terrible that someone saw their pension fall to just £3,000, they made that decision and accepted the risks.

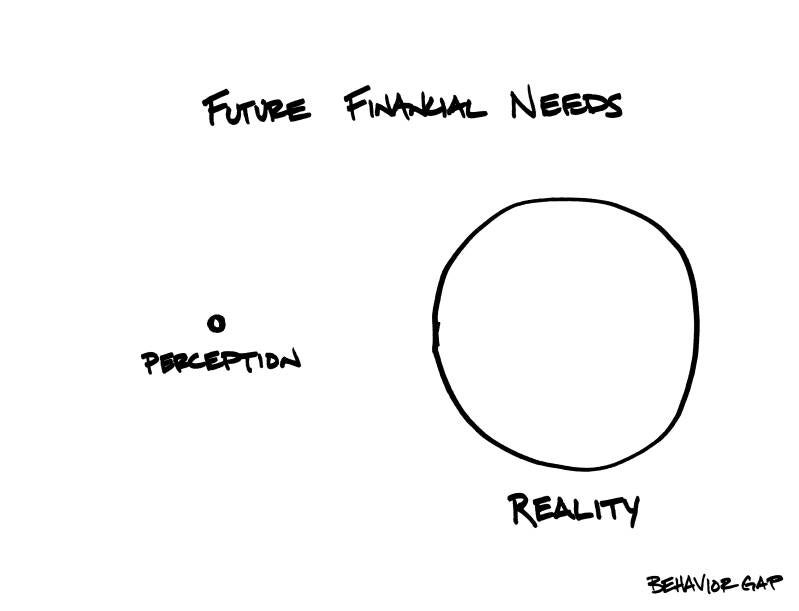

This is an excellent place to start from Behaviorgap.

The point is simple: a financial planner (adviser) is there to sit in the middle.

If we put “value” back into the equation, we can ask whether we consider this as value.

What to expect

This blog will not attempt to explain in detail the value of advice. Some fantastic books would explain it much better than any blog I write.

However, it is worth understanding what a financial planner can offer. For many just starting, there is no need to employ the services of a financial planner. Still, life can become complicated, especially when you come into an unexpected amount of money.

A financial planner is more than someone who sells a product. It is about understanding you, your needs, wants, and desires. I like this illustration, which shows that our finances can be complex.

A complex mess can lead to mistakes.

Most financial planners will talk about plans.

And this is the crux of everything. We all have dreams and aspirations, but can we achieve them? Just investing money with no plan makes very little sense.

Is a 1% p.a. fee expensive? Well, that depends. A good financial planner will look after you; rightly, the FCA is checking to see if financial planners are delivering on their promises. It is about trust and what you are comfortable with to some extent. Every financial planner has to make a profit, and running a practice is not cheap, but if someone is subsidising the business, there may be questions about this.

The litmus test is whether I personally have a financial planner and why.

The simple answer is yes: before instructing one, I spent too much time focusing on the investments without having a plan in place, meaning I lost more than I made. Is it right for everyone?.....That depends. But when we see the dangers of people who invest their own money and lose it all, perhaps it highlights the need for some, and rather than being focused on the 1% per annum fee, we should concentrate on what they offer and then ensure that they deliver on that.

Add comment

Comments